The Legal Framework of Corporate Spin-Offs and Divestitures

An elite guide on corporate best practices.

Advertisement

In today's dynamic corporate environment, stasis is the precursor to decline. The modern conglomerate, once a symbol of industrial might, now faces persistent pressure from activist investors, capital markets, and rapidly shifting technological paradigms to become more agile, focused, and efficient. In this context, corporate spin-offs and divestitures have evolved from mere financial engineering into indispensable instruments of corporate strategy. They are the crucibles in which shareholder value is refined, non-core assets are monetized, and newly independent entities are forged to pursue their own distinct growth trajectories.

However, the path from a strategic decision to divest to a successfully executed transaction is fraught with immense legal and regulatory complexity. A spin-off is not simply a sale; it is the intricate de-integration of a living, breathing business unit from its corporate parent. This process touches upon nearly every facet of corporate law, from the fiduciary duties of the board and the stringent requirements of tax-free treatment to the nuanced compliance demands of securities regulations and the delicate management of human capital. Executing this maneuver requires more than just financial acumen; it demands a sophisticated, multi-disciplinary legal strategy orchestrated with surgical precision.

This authoritative guide, prepared by the senior corporate strategy and legal counsel at Jurixo, serves as a comprehensive roadmap for boards of directors, C-suite executives, and in-house legal teams contemplating or executing a corporate separation. We will dissect the critical legal pillars that form the foundation of any successful spin-off or divestiture, providing the strategic clarity necessary to navigate this complex terrain and transform a strategic vision into a value-creating reality.

Differentiating Strategic Divestitures: Spin-Offs, Split-Offs, and Equity Carve-Outs

Before delving into the legal intricacies, it is crucial to establish a precise definitional framework. While often used interchangeably in business parlance, the primary methods of corporate separation have distinct structural, tax, and shareholder implications.

-

Spin-Off: This is the most common form of divestiture. The parent company ("ParentCo") distributes shares of a subsidiary ("SpinCo") to its existing shareholders on a pro-rata basis. No cash is raised. After the transaction, ParentCo shareholders own shares in two separate, publicly traded companies. The goal is typically to create two more-focused businesses, which the market may value more highly apart than together.

-

Split-Off: This transaction is structured as an exchange offer. ParentCo offers its shareholders the option to exchange their ParentCo shares for shares of SpinCo. This is a non-pro-rata distribution, as only the shareholders who choose to participate will receive SpinCo stock. This method is often used when there is a desire to consolidate the ownership of either ParentCo or the departing SpinCo.

-

Equity Carve-Out (or Partial IPO): In a carve-out, ParentCo sells a percentage of its equity in SpinCo to the public through an Initial Public Offering (IPO). ParentCo receives cash proceeds from the sale and typically retains a controlling stake in the newly public SpinCo. This is often a precursor to a full spin-off, allowing ParentCo to raise capital while establishing a public market valuation for SpinCo before distributing the remaining shares.

The choice between these structures is a foundational strategic decision driven by the parent company’s objectives: Is the goal to deliver a pure-play investment to existing shareholders (spin-off), consolidate a shareholder base (split-off), or raise capital and establish a market price (carve-out)? This initial choice dictates the entire legal and transactional path forward.

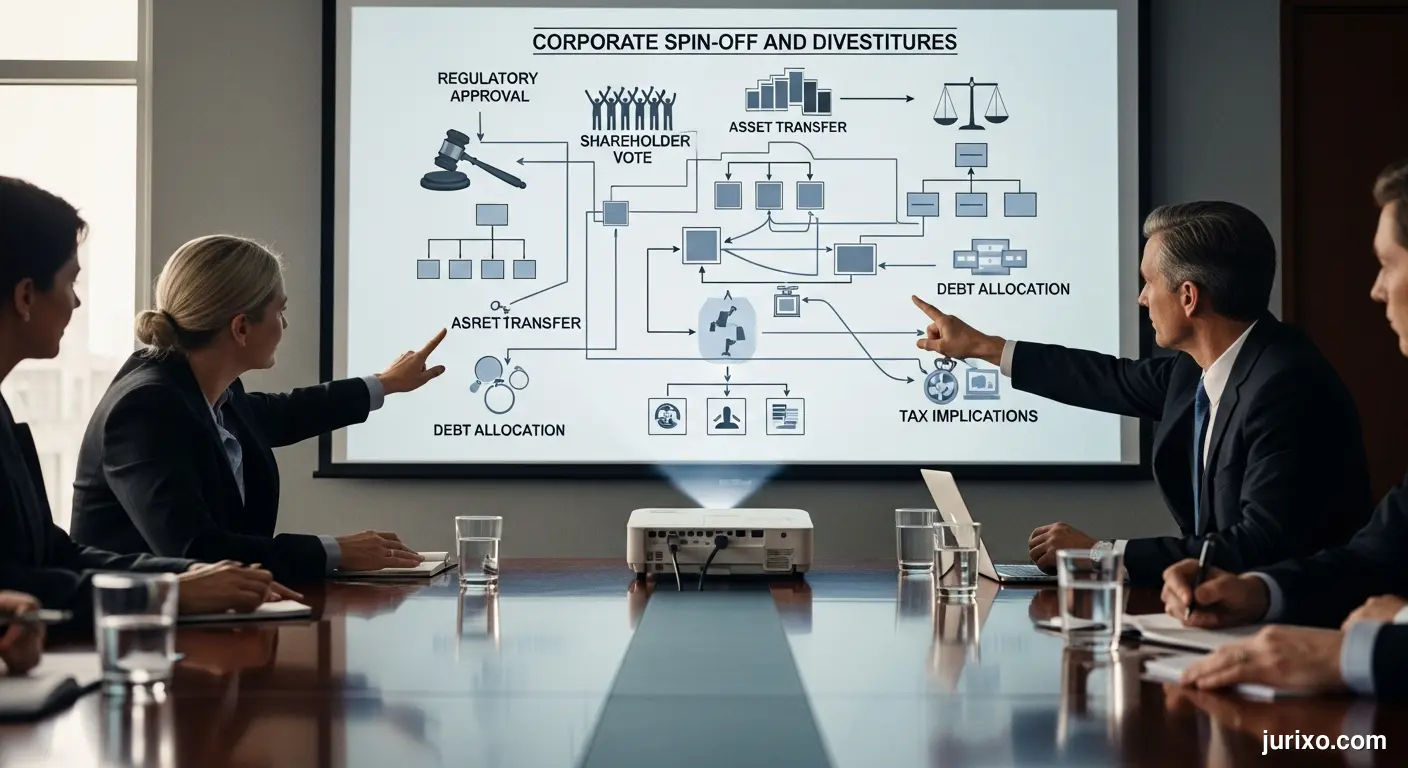

The Core Legal Pillars of a Divestiture Transaction

A successful divestiture is built upon several interlocking legal pillars. Failure to adequately address any one of them can lead to value destruction, shareholder litigation, adverse tax consequences, or regulatory sanction.

Pillar 1: Corporate Law and Fiduciary Duties

The decision to pursue a spin-off rests squarely with the board of directors of ParentCo. This decision, like any major corporate action, is governed by the board's fundamental fiduciary duties of care and loyalty to the corporation and its shareholders.

The Duty of Care requires directors to be fully informed and to act with the diligence that a reasonably prudent person would in a similar position. In the context of a spin-off, this means the board must:

- Thoroughly evaluate the strategic rationale for the separation.

- Engage qualified financial advisors to conduct a rigorous valuation and solvency analysis.

- Consider and analyze the potential impacts on both ParentCo and the future SpinCo.

- Review and understand the proposed terms of the separation, including intercompany agreements.

The Duty of Loyalty requires directors to act in good faith and in the best interests of the corporation, free from conflicts of interest. This is particularly salient if directors or officers have a personal financial interest in the success of SpinCo over ParentCo (or vice-versa), for instance, through post-spin compensation arrangements.

Provided the board acts on an informed basis, in good faith, and without self-interest, its decision will typically be protected by the Business Judgment Rule. This legal doctrine presumes that directors have acted in the best interests of the company, and courts will generally not second-guess their decisions. Meticulous record-keeping, documented in board minutes, is essential to demonstrate that the board has fulfilled its duties and can rely on this protection.

Pillar 2: The Tax Implications – Section 355 and Beyond

Perhaps the most complex and valuable aspect of a spin-off's legal structure is its potential to be completely tax-free to both the parent corporation and its shareholders. This coveted treatment is governed by Section 355 of the U.S. Internal Revenue Code. Failing to meet its stringent requirements can transform a value-accretive transaction into a catastrophic tax liability.

To qualify for tax-free treatment under Section 355, as detailed by the Cornell Law School Legal Information Institute, a transaction must satisfy a series of rigorous tests:

- Control Requirement: ParentCo must "control" SpinCo immediately before the distribution. Control is defined as owning at least 80% of the total combined voting power and at least 80% of the total number of shares of all other classes of stock.

- Distribution of Control: ParentCo must distribute either all of its stock and securities in SpinCo or an amount of stock constituting control, and establish to the satisfaction of the IRS that retaining any stock was not for tax-avoidance purposes.

- Active Trade or Business (ATB) Requirement: This is a critical hurdle. Both ParentCo and SpinCo must be engaged in the "active conduct of a trade or business" immediately after the distribution. Furthermore, this business must have been actively conducted for the five-year period ending on the date of the distribution.

- Corporate Business Purpose Doctrine: The transaction must have a valid, non-federal-tax corporate business purpose. Examples include enhancing shareholder value, improving access to capital markets for both entities, resolving management or systemic problems, or enabling a better fit and focus. This purpose must be substantiated and documented.

- Continuity of Interest (COI): The pre-distribution shareholders of ParentCo must maintain a sufficient continuing equity interest in both ParentCo and SpinCo after the separation.

- Device Test: The transaction cannot be used principally as a "device" for the distribution of earnings and profits. This test is intended to prevent transactions that are functionally equivalent to a taxable dividend.

Navigating these requirements is a high-stakes exercise. The parent company will typically seek a private letter ruling (PLR) from the IRS or, more commonly today, a formal tax opinion from its legal counsel confirming that the transaction "should" or "will" qualify under Section 355.

Pillar 3: Securities Law Compliance

When a spin-off creates a new public company, it triggers significant obligations under U.S. securities laws, primarily those administered by the Securities and Exchange Commission (SEC). The goal is to ensure that the market and the shareholders receiving SpinCo stock have access to complete and accurate information about the new entity.

For a spin-off, this is typically achieved by filing a Form 10 Registration Statement with the SEC. Unlike an IPO registration (Form S-1), a Form 10 does not register an offering of securities for sale; rather, it registers the class of SpinCo securities that will be distributed. The Form 10 contains extensive information about SpinCo, including:

- Detailed Business Description: A thorough overview of SpinCo's operations, products, markets, and competitive landscape.

- Risk Factors: A candid and comprehensive discussion of the risks specific to SpinCo's business and its status as a newly independent company.

- Management's Discussion and Analysis (MD&A): A narrative explanation of SpinCo's financial performance.

- Carve-Out Financial Statements: Audited historical financial statements for the SpinCo business, "carved out" from ParentCo's consolidated financials. This is often one of the most time-consuming aspects of the entire process.

- Pro Forma Financials: Financial statements showing how the separation will impact SpinCo's financial position.

- Executive Compensation and Corporate Governance: Details on the new board and management team, and their compensation structure.

The Form 10 is filed with the SEC and undergoes a review and comment process. Once the SEC has no further comments, the Form 10 becomes "effective," and ParentCo can proceed with the distribution. The Information Statement, which is the primary disclosure document sent to shareholders, is an integral part of the Form 10. For more information on public filings, the SEC's EDGAR database provides access to thousands of such documents.

Pillar 4: Employee, Benefits, and Compensation Issues

A corporate separation is a deeply human event. The legal framework must carefully manage the transition of employees and the division of compensation and benefit plans.

Key considerations include:

- Employee Allocation: Determining which employees will transfer to SpinCo and which will remain with ParentCo. This involves navigating employment laws, collective bargaining agreements, and potential transfer-of-undertakings regulations in non-U.S. jurisdictions.

- Benefits Plan Separation: Employee benefit plans, such as 401(k)s, pension plans, and health and welfare plans, must be separated. This may involve creating mirror plans at SpinCo, transferring assets between plans, and ensuring compliance with the Employee Retirement Income Security Act (ERISA).

- Treatment of Equity Awards: A critical and often complex task is determining how to treat outstanding ParentCo equity awards (stock options, RSUs, PSUs) held by both transferring and remaining employees. The typical approach is to adjust the awards to preserve their intrinsic value, resulting in holders receiving awards in both ParentCo and SpinCo post-separation.

- New Executive Compensation: The new SpinCo will need its own executive compensation structure. As our firm details in its guide on "Designing Executive Compensation Packages: Legal and Tax Perspectives," this involves benchmarking against a new peer group and aligning incentives with the strategic goals of the standalone company.

Pillar 5: Operational Separation and Contractual Matters

The legal de-integration must be matched by an operational one. SpinCo must be able to operate as a standalone entity from Day One. This requires a forensic review of all operational entanglements and the drafting of key agreements to govern the post-separation relationship.

The most important of these is the Separation and Distribution Agreement, which serves as the master blueprint for the entire transaction. It outlines the assets and liabilities being transferred to SpinCo, the mechanics of the distribution, and the conditions to closing.

Supporting this master agreement are several crucial ancillary agreements:

- Transitional Services Agreement (TSA): It is rarely possible for SpinCo to replicate all of ParentCo's corporate functions (e.g., IT, HR, finance) immediately. A TSA is a contract where ParentCo agrees to provide these services to SpinCo for a specified period (e.g., 6-24 months) in exchange for a fee, giving SpinCo time to build its own infrastructure.

- Tax Matters Agreement: This agreement governs the respective rights and obligations of ParentCo and SpinCo with respect to taxes, including liability for taxes arising before and after the spin, and covenants designed to protect the tax-free status of the transaction.

- Employee Matters Agreement: This codifies the agreements regarding the allocation of employees and the treatment of compensation and benefit plans.

- Intellectual Property Agreements: If ParentCo and SpinCo will both need to use shared intellectual property, cross-licensing agreements must be put in place.

Navigating Regulatory Hurdles and Antitrust Considerations

While a "pure" spin-off (a pro-rata distribution to existing shareholders) does not typically trigger pre-merger notification requirements under the Hart-Scott-Rodino (HSR) Act in the United States, the legal analysis is not always straightforward. Certain complex structures, particularly those involving a significant pre- or post-spin acquisition by a third party (a so-called "Reverse Morris Trust" transaction), can trigger HSR filing obligations.

Furthermore, if the divestiture takes the form of a sale to a specific buyer rather than a spin-off to shareholders, a full antitrust review is almost certain. This involves a deep analysis of market definition, concentration, and potential anti-competitive effects. As we've noted in other contexts, Navigating Antitrust Regulations During Industry Consolidation is a specialized discipline that requires expert counsel from the outset.

Regulators such as the Federal Trade Commission (FTC) will scrutinize transactions that could lessen competition in a given market. Therefore, even in a spin-off, the board must consider the broader competitive landscape, especially if the separation is part of a larger strategic plan involving future M&A.

Conclusion: The Strategic Imperative of Expert Counsel

The legal framework governing corporate spin-offs and divestitures is a mosaic of corporate, tax, securities, employment, and contract law. Each piece must be perfectly placed to ensure the transaction achieves its strategic objectives without incurring unforeseen liabilities. The process is a marathon, not a sprint, often taking 12-18 months from conception to completion.

For boards and executive teams, the message is clear: proactive, integrated legal and strategic advice is not a cost center—it is the fundamental enabler of a successful separation. From structuring the transaction to achieve tax-free status, to navigating the SEC review process, to drafting the intricate web of intercompany agreements, expert counsel is the thread that binds the entire endeavor together. At Jurixo, we partner with our clients to transform the immense complexity of a corporate separation into a clear, actionable, and value-creating strategic execution.

Frequently Asked Questions (FAQ)

1. What is the single biggest mistake boards make when contemplating a spin-off? The most significant error is underestimating the operational complexity and time required for a clean separation. Boards often focus heavily on the financial and strategic rationale but fail to appreciate the immense effort needed to untangle shared services, IT systems, supply chains, and intellectual property. This leads to unrealistic timelines, budget overruns, and a poorly executed Transitional Services Agreement (TSA) that can cripple the new SpinCo or burden the ParentCo post-separation. A successful spin requires a dedicated project management office and operational workstreams to begin work in parallel with the legal and financial workstreams from day one.

2. How do we manage market perception and communication during a lengthy spin-off process? A disciplined communication strategy is paramount. The initial announcement should clearly articulate the compelling strategic rationale for the separation and the value it is expected to unlock for shareholders of both future companies. Following the announcement, a "quiet period" may be necessary, but it is crucial to maintain regular communication with key stakeholders. This includes tailored messaging for investors (highlighting financial profiles), employees (addressing uncertainty and career paths), and customers/suppliers (ensuring continuity of service). A dedicated investor relations and corporate communications plan, developed with legal counsel to ensure compliance with securities laws, is essential to control the narrative and prevent value erosion due to uncertainty.

3. What is a "Reverse Morris Trust" transaction and why is it so legally complex? A Reverse Morris Trust (RMT) is a highly sophisticated, tax-efficient structure that combines a spin-off with a pre-arranged merger. In a typical RMT, ParentCo spins off SpinCo, which then immediately merges with an interested acquiring company. The structure is designed so that the former ParentCo shareholders own more than 50% of the newly combined entity. If structured correctly under Section 355, the spin-off and the merger can be tax-free. The complexity arises from navigating the "anti-Morris Trust" rules, which are designed to prevent disguised corporate sales. This requires meticulous planning around the timing, valuation, and control of the combined entity, along with intense scrutiny from a tax, securities, and often antitrust perspective.

4. How do we determine the right capital structure for SpinCo? Determining SpinCo's Day One capital structure is a critical exercise in financial and legal strategy. It is not simply an accounting function. The board, with its financial advisors, must model a structure that allows SpinCo to thrive as a standalone entity. This involves assessing its ability to service debt, fund its growth initiatives, and achieve a target credit rating. Typically, ParentCo will seek to "load" SpinCo with a certain amount of debt, the proceeds of which are often transferred to ParentCo as a tax-free dividend immediately before the spin. However, overburdening SpinCo with debt can hamstring its future and invite shareholder litigation. The board's fiduciary duties require a balanced approach that is defensible as being in the best interests of both companies and their respective shareholders.

5. Beyond the TSA, what is the most contentious agreement to negotiate between ParentCo and SpinCo? The Tax Matters Agreement is frequently the most heavily negotiated ancillary document. This agreement is the definitive word on which company is responsible for taxes pre- and post-spin, who controls tax audits, and, most importantly, which party bears the catastrophic financial risk if the spin-off is later determined by the IRS to be taxable. The agreement includes powerful covenants that restrict both ParentCo and SpinCo from taking certain actions (like issuing significant equity or ceasing an active business) for a two-year period post-spin, as such actions could retroactively disqualify the tax-free treatment. The indemnification clauses for a breach of these covenants are a major point of contention and require sophisticated legal and tax counsel to negotiate effectively.

Advertisement

Last Updated: